Supermarket News is part of the Informa Connect Division of Informa PLC

INFORMA PLC

|

ABOUT US

|

INVESTOR RELATIONS

|

TALENT

This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

About Us

Subscribe

Advertise

Webinars

Sign Up

Sign Up

Grocery Operations

Related Topics

Grocery Technology

Legislation & Regulatory News

Mergers & Acquisitions

Independents / Regional Grocers

Grocery Marketing

Grocery Wholesale & Distributors

Retail Labor

Foodservice at Retail

Food Safety

Sustainability

Grocery Pharmacy & Health Care

Finance

New Stores

Executive Moves

Supplier News

Company News

Store Closings

Recalls

Retail Media

Food Accessibility

Recent in

Grocery Operations

See All

A Walgreens storefront with the 5 things top news logo in the upper right corner.

Grocery Operations

5 things top news: Walgreens’ slide continues

5 things top news: Walgreens’ slide continues

by

Bill Wilson

Oct 21, 2024

A seafood display at a grocery store

Seafood

How to become a peerless seafood prognosticator

How to become a peerless seafood prognosticator

by

Richard Mitchell

Oct 14, 2024

4 Min Read

Grocery Trends & Data

Related Topics

Consumer Trends

Health & Wellness

Organic & Natural

CPG

New CPG Products

Recent in

Grocery Trends & Data

See All

thumbnail

Grocery Trends & Data

The Retail Daily podcast

The Retail Daily podcast

Oct 21, 2024

A slice of pumpkin pie with whipped cream on top.

Grocery Trends & Data

Report: Grocers capitalize on pumpkin flavor

Report: Grocers capitalize on pumpkin flavor

by

Bill Wilson

Oct 17, 2024

1 Min Read

Grocery Categories

Related Topics

Bakery

Beverages

Nonfood & Pharmacy

Fresh Produce

Deli

Prepared Foods

Meat

Seafood

Dairy

Center Store

Frozen

Private Label

HBC Health & Beauty

Recent in

Grocery Categories

See All

A blurred picture of a frozen food section in a grocery store.

Grocery Categories

Category update: Nature and manmade disasters help with September food sales

Category update: Nature and manmade disasters help with September food sales

by

Bill Wilson

Oct 16, 2024

7 Min Read

A seafood display at a grocery store

Seafood

How to become a peerless seafood prognosticator

How to become a peerless seafood prognosticator

by

Richard Mitchell

Oct 14, 2024

4 Min Read

Sponsored By

Home

Documents

Documents

thumbnail

Organic & Natural

The big picture: Natural and organic industry sales data for 2023

The big picture: Natural and organic industry sales data for 2023

by

Douglas Brown

Sep 5, 2024

1 Min Read

15520-Supermarket_News-2400x800_v3.jpg

Sponsored Content

Simplifying CO2 refrigeration management with integrated controls

Simplifying CO2 refrigeration management with integrated controls

Aug 8, 2024

1 Min Read

All Documents

Sponsored Content

Tasty Fresh boosts efficiency by 35% with voice technology

Tasty Fresh boosts efficiency by 35% with voice technology

Mar 25, 2024

|

1 Min Read

Sponsored Content

Securing Business Growth with Ice

Securing Business Growth with Ice

Dec 22, 2023

|

1 Min Read

Sponsored Content

How Top Brands Boost Loyalty with Product Transparency

How Top Brands Boost Loyalty with Product Transparency

Dec 20, 2023

|

1 Min Read

Sponsored Content

Bringing A2L Technology to the Forefront of Commercial Refrigeration

Bringing A2L Technology to the Forefront of Commercial Refrigeration

Dec 1, 2023

|

1 Min Read

Sponsored Content

2023 Fresh Foods Survey from Supermarket News

2023 Fresh Foods Survey from Supermarket News

Aug 3, 2023

|

1 Min Read

Sponsored Content

CO2 Refrigeration With Confidence

CO2 Refrigeration With Confidence

Feb 15, 2023

|

1 Min Read

Sponsored Content

Building a bridge to alternative energies for supermarket transportation

Building a bridge to alternative energies for supermarket transportati

Aug 19, 2022

|

1 Min Read

Grocery Trends & Data

2022 Fresh Foods Survey from Supermarket News

2022 Fresh Foods Survey from Supermarket News

Jul 14, 2022

|

1 Min Read

Sponsored Content

The Recipe to Combat Inflation: Fresh Intelligent Forecasting

The Recipe to Combat Inflation: Fresh Intelligent Forecasting

May 2, 2022

|

1 Min Read

Sponsored Content

Grocery Order Picking Solutions from OPI

Grocery Order Picking Solutions from OPI

Apr 26, 2022

|

1 Min Read

Finance

Grocery Retailer Expectations for 2022

Grocery Retailer Expectations for 2022

Mar 30, 2022

|

1 Min Read

Consumer Trends

Trends & Predictions for 2022

Trends & Predictions for 2022

Feb 1, 2022

|

1 Min Read

Consumer Trends

Top Grocery Trends of 2021

Top Grocery Trends of 2021

Sep 8, 2021

|

1 Min Read

Sponsored Content

How robots help retailers meet today’s cleaning challenges

How robots help retailers meet today’s cleaning challenges

Jun 22, 2021

|

1 Min Read

Sponsored Content

Retail buyer’s guide to robotic floor scrubbers

Retail buyer’s guide to robotic floor scrubbers

Jun 14, 2021

|

1 Min Read

Sponsored Content

2021 Fresh Foods Survey from Supermarket News

2021 Fresh Foods Survey from Supermarket News

Jun 10, 2021

|

1 Min Read

Sponsored Content

Retail buyer’s guide to robotic floor scrubbers update from May 2021

Retail buyer’s guide to robotic floor scrubbers

May 4, 2021

|

1 Min Read

Sponsored Content

Are you ready to comply with NBFDS?

Are you ready to comply with NBFDS?

Apr 28, 2021

|

1 Min Read

Sponsored Content

The hidden problem ruining grocer profits

The hidden problem ruining grocer profits

Mar 22, 2021

|

1 Min Read

Finance

Surviving a Food Contamination Crisis: Creating a Successful Financial Recovery Strategy

Surviving a Food Contamination Crisis: Creating a Successful Financial

Aug 24, 2020

|

1 Min Read

Sponsored Content

The robotics revolution in the grocery industry

The robotics revolution in the grocery industry

May 20, 2020

|

1 Min Read

Consumer Trends

New Approaches to Key Retail Categories

New Approaches to Key Retail Categories

May 8, 2020

|

1 Min Read

Foodservice at Retail

5 Ways to work smarter in today’s retail market

5 Ways to work smarter in today’s retail market

Apr 27, 2018

|

1 Min Read

Sponsored Content

See how to keep your checkout lines moving

See how to keep your checkout lines moving

Oct 3, 2017

|

1 Min Read

Grocery Operations

The Biggest P&L Line Item You’re Not Paying Enough Attention To

The Biggest P&L Line Item You’re Not Paying Enough Attention To

Apr 23, 2015

|

1 Min Read

Grocery Categories

Grocery Channel: Premium is the New Mass Market

Grocery Channel: Premium is the New Mass Market

Mar 4, 2015

|

1 Min Read

Grocery Trends & Data

SN Price Check: Houston update from July 2014

SN Price Check: Houston

Jul 23, 2014

|

1 Min Read

Grocery Trends & Data

Infographic: Recipe trends across generations

Infographic: Recipe trends across generations

Apr 8, 2014

|

1 Min Read

CPG

IRI Infographic: The formula for high-octane CPG fuel

IRI Infographic: The formula for high-octane CPG fuel

Mar 12, 2014

|

1 Min Read

Grocery Trends & Data

Store Brands 2014: Sales Trends

Store Brands 2014: Sales Trends

Jan 27, 2014

|

1 Min Read

Grocery Trends & Data

Supermarket Industry Salary Table

Supermarket Industry Salary Table

Oct 25, 2013

|

1 Min Read

Grocery Trends & Data

Aug. 12, 2013: More Retail M&A Ahead: Report

Aug. 12, 2013: More Retail M&A Ahead: Report

Aug 12, 2013

|

1 Min Read

Grocery Trends & Data

June 17, 2013: Wal-Mart Logistics Statistics

June 17, 2013: Wal-Mart Logistics Statistics

Jun 17, 2013

|

1 Min Read

Previous

1

2

Next

Read more

The front of a Walmart store showing the Walmart logo.

Nonfood & Pharmacy

Walmart now delivers prescription drugs in select states

Walmart now delivers prescription drugs in select states

A Target bullseye sign on the outside of a store.

Company News

Target engages in another round of price cuts, this time involving more than 2,000 items

Target engages in another round of price cuts, this time involving more than 2,000 items

SNAP sign

Legislation & Regulatory News

Walmart takes more than 25% of all SNAP dollars

Walmart takes more than 25% of all SNAP dollars

A CVS storefront.

Retail Labor

Los Angeles-area CVS workers are back on the job, while Rite Aid employees authorize strike

Los Angeles-area CVS workers are back on the job, while Rite Aid employees authorize strike

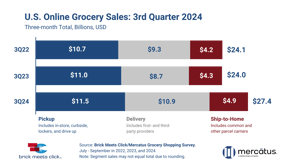

Brick Meets Click statistics

Grocery Technology

Walmart continues growing its share of online grocery dollars

Walmart continues growing its share of online grocery dollars

Stay up-to-date on the latest food retail news and trends

Subscribe to free eNewsletters from Supermarket News

Sign Up Now